Corn exports continue to lag

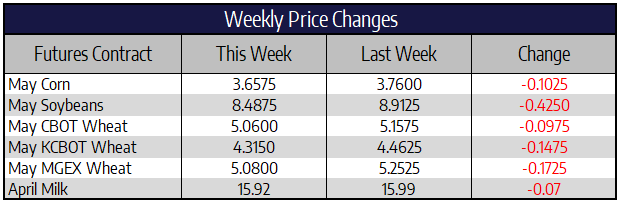

Despite the blowout weakness in most other markets this week, the corn market held up relatively well. May corn closed at 365-3/4 down 10-1/4 cents this week. December corn was down 8-1/2 cents this week to close at 373 down 8-1/2 cents this week. According to US Census Bureau statistics published on Friday, January corn exports totaled 2.49 million tons, some 34% below the recent five-year average. Cumulative shipments for the first five months of the 2019-20 marketing year now total 11.8 million tons, a seven-year low. The recent US marketing years in which corn sales started out very slowly ended with a flurry of sales and exports after South American harvest fell short. That happened in both 2015-16 and 2017-18, but USDA on Tuesday kept production in Brazil and Argentina at 101 million and 50 million tons, respectively, record or near-record large. Down in Brazil second crop corn nationwide is 75-80% planted and generally the planting ends about March 10th to the 15th but record high domestic corn prices may encourage farmers to plant their safrinha corn later than recommended this year. China has published a list of 88 US suppliers that can export distillers dried grains (DDGs) to the country, according to the General Administration of Customs. China used to be the largest purchaser of US DDGs. Imports hit a peak of 6.5 million tons in 2015. The market will be watching for purchase of any corn or corn products by China in the near term as well as looking ahead to the planting intentions report at the end of the month.

Soybeans close into six-month lows

May Chicago soybean futures had an awful week, trading 42-1/2 cents lower this week closing at 848-3/4. November soybean futures closed the week at 864-1/2 down 41 cents. Chicago soybean futures slid to a six-month low this week on the threat of deeper economic damage from the coronavirus, dragging down global stocks and commodities. Strength in the stock market during the day on Friday may be seen as a positive that the tide has turned somewhat in the overall marketplace. Meal demand has been building around the world for the past few years with increasing livestock demand. However, hog and cattle prices fell through the floor this week trading to new contract lows. With the cancellation of large gatherings in the US and around the world amid the coronavirus outbreak an overall hit to global protein consumption may be on the horizon. The ripple effect of backed up livestock supply chains could put increased pressure on the commodity sector as a whole. Adding to price pressure was the US dollar vs the Brazilian real which made new record highs this week as the real continued its weakness. As of late last week, soybean harvest in Mato Grosso was seen as 91% complete. Mato Grosso is Brazil’s largest soybean producing state accounting for nearly a 1/3 of Brazil’s soybeans.

Chicago wheat continues lower

May Chicago wheat was 9-3/4 cents lower this week to close at 506. May KC wheat was 14-3/4 cents lower to close at 431-1/2. May spring wheat closed the week at 508 down 17-1/4 cents this week. The wheat market followed all other markets lower this week. Excessive rainfall over Germany and French growing areas over the past month could lead to a decline in EU soft wheat production. Export sales were in line with estimates this week. Net wheat sales came in at 480,000 tons, traders were expecting between 200 and 600 thousand tons. Like most other markets, the wheat market now sits in oversold territory. Resistance looks to be near the 512 area on May Chicago wheat while support may come in around the 490 mark.

Block/Barrel Average Jumps 3.625 cents

When looking at how outside markets responded to the coronavirus this week, the dairy spot trade held impressively well. The cheese was actually able to finish 7.25 cents higher on the block/barrel average this week as cheese moved into a strong area of support at $1.60/lb. Whey prices were quiet this week, finishing unchanged. The class IV products continue to be most susceptible to the price decline in outside markets. Butter dropped 4.25 cents on the week, but was up 13 cents last week. Powder prices lost all 5 cents of last week’s gains and then some dropping 6.25 cents on the day.

Price action continues to move lower in the futures market for Class III despite the recent rise in cheddar prices in the spot market. The outside pressures are clearly keeping futures optimism limited recently. With Class IV prices it is even more so given the decline in powder and butter prices this week. There will be a Global Dairy Trade auction coming on Tuesday of next week. There have been three down auctions in a row and it will be interesting to see if lack of new virus news from China is making things better.

Author

Lisa Heder