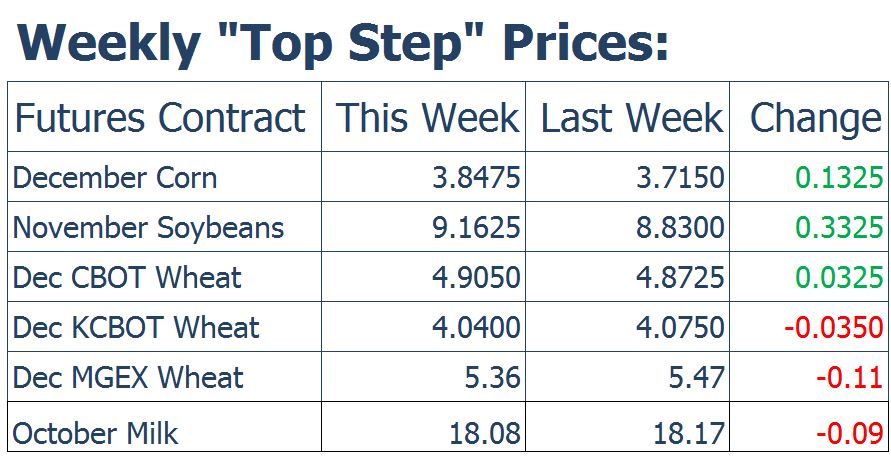

Corn had its biggest weekly rally since June.

December corn futures closed 4 cents lower today but finished the week 13-1/4 higher at 384-3/4 as a surprisingly lower quarterly stocks report on Monday lifted prices. However, the market gave back some of the gains despite an announcement on biofuels from the White House today and corn slid lower into the close. The USDA’s Quarterly Stocks report pegged corn stocks at 2.114 billion bushels, below the average trade guess of 2.428 billion and down 1% from a year ago. The September Supply and Demand report had ending stocks at 2.45 billion meaning the USDA could still lower ending stocks for 2018/2019 by 300 million thus lowering the new crop carryout. This is friendly to price and moved corn 16 cents higher that day. Despite lower supplies, export sales and shipments continue to come up short of the pace need to reach USDA targets and could offset some of the supply decline.

The Trump administration today unveiled a plan to boost U.S. biofuels consumption in 2020. Details were light but the plan involves an unspecified increase in the 2020 blend requirement and a push for the sale of higher ethanol blends of gasoline like E15. It does not involve a repeal of blend waivers that has angered the ethanol industry.

Soybeans rally on lower supplies.

Soybeans were up sharply this week. November soybean futures closed up 4-1/2 today at 916-1/4, up 33-1/4 for the week. The contract closed above the 200-day moving average for the first time since mid-July. Soybeans surged higher after the USDA released its Quarterly Stocks report showing supplies in all locations down more than expected at 913 million bushels. This is below the average of analysts guesses and below the USDA’s September supply and Demand ending stock number of 1.005 billion bushels. The USDA took the added step of adjusting production for the 2018/2019 crop year on this report. Production was lowered 4.428 billion. The agency commented that the reduction of 116 million bushels is based on the latest stocks number, crush data and information from farm programs. Harvested area was lowered 500,000 acres and yield lowered 1 bushel per acre to 50.6 bpa. This would lower ending stocks to 524 million. Half what we thought they could be back in March. The stocks to use at 13% while not historically tight is a lot lower than last season and would suggest prices should move higher. China has purchased more than 130 million bushels of soybeans so far this marketing year versus 47 million by this time last year but cumulative sales still lag last year by 29 percent.

Wheat prices mostly lower.

Wheat futures were mixed this week. Winter wheats fared better on a friendly USDA report while Spring wheat gave back some of its recent gains. For the week, Chicago December gained 3-1/4 cents at 490-1/2, KC was down 3-1/2 at 4.04, while Minneapolis was down 11 cents to 536. The USDA Quarterly Stocks down 5 million bushels from last year at this time at 2.385 billion bushels however this was well above the average trade guesses at 2.318 billion. Wheat production at 1.962 billion bushels is down 18 billion from the August estimate and slightly below expectations. This was mostly due to a reduction in soft red winter wheat. US exporters announced a sale of almost 5 million bushels of white wheat to China this week. This was the largest single wheat sale to China since 2016.

Class III Pulls Back as Cheese Prices Stall in the Spot Market

After five up days in a row, the spot cheese markets advance was halted. The block/barrel average finished the day 0.375 cents lower as Barrels gained 2 cents and Blocks lost 2.75 cents. The spread between the two has gone from 40 cents to 20.25 cents in a little over a week. Whey prices dropped 1.25 cents to $0.3275 cents trading over 80 loads traded on the week. A phenomenal amount for the whey market. Butter prices remained steady at $2.185/lb the high of the week. The non-fat powder market continues its impressive advance as it finishes at a new high for the year for the second week in a row.

Class III futures are currently retesting the $18.00 dollar level on the 2nd month contract again as the low for the day on November was $18.00 on the dot. The market continues to support prices at that level. The market trade was pretty pessimistic today at the slight drop in spot cheese prices seems to be pressuring the market lower. Perhaps traders are concerned the spread between blocks and barrel prices will continue to decrease from a lower block price.

Author

Carol Tillmann